Not 21 Yet?

As of the Credit Card act of 2009, no one under the age of 21 can attain a credit card account without the co-sign of an adult. The only exception to this rule is if the applicant can prove they pay their own bills. There are three options to consider and look over when discussing with your parent/guardian on how to get a credit card.

Co-Sign:

This is the only way an 18-year-old can sign up for a credit card account. With this option, the applicant not the parent/guardian will receive the credit card statement. The applicant is also responsible for paying the bill on time. This is easily done either by mailing a check in by the due date, or simply paying online through online banking.

Joint Account:

With this option, the parent/guardian opens a new credit card account and adds their child as a joint user. Parents/guardians don’t need to worry about their child missing the payments as they make the payments themselves. Another benefit is that the child will benefit from sharing your hopefully good credit history, thereby boosting their credit score. The only downside is the child isn’t paying their bill and aren’t getting the experience of managing their own account.

Authorized User:

This involves adding the child as an authorized user on the parent/guardians credit card. While it looks and feels similar to the Joint Account, the main difference is who the bank views as the main card holder. In this case it is the parent/guardian. It’s important to be aware that some companies will charge a fee for adding an additional user. Should the goal be to increase the child’s credit score, then this is not the desired option. As an authorized user they are not able to benefit as much as they would via a joint account.

What you and your parent/guardian choose is entirely up to you. Be sure to talk this over with them before applying for a card. Also be sure to discuss whether or not you need a card. Having a card and being irresponsible with spending and paying back the balance can hurt your finances in years to come.

Co-Sign:

This is the only way an 18-year-old can sign up for a credit card account. With this option, the applicant not the parent/guardian will receive the credit card statement. The applicant is also responsible for paying the bill on time. This is easily done either by mailing a check in by the due date, or simply paying online through online banking.

Joint Account:

With this option, the parent/guardian opens a new credit card account and adds their child as a joint user. Parents/guardians don’t need to worry about their child missing the payments as they make the payments themselves. Another benefit is that the child will benefit from sharing your hopefully good credit history, thereby boosting their credit score. The only downside is the child isn’t paying their bill and aren’t getting the experience of managing their own account.

Authorized User:

This involves adding the child as an authorized user on the parent/guardians credit card. While it looks and feels similar to the Joint Account, the main difference is who the bank views as the main card holder. In this case it is the parent/guardian. It’s important to be aware that some companies will charge a fee for adding an additional user. Should the goal be to increase the child’s credit score, then this is not the desired option. As an authorized user they are not able to benefit as much as they would via a joint account.

What you and your parent/guardian choose is entirely up to you. Be sure to talk this over with them before applying for a card. Also be sure to discuss whether or not you need a card. Having a card and being irresponsible with spending and paying back the balance can hurt your finances in years to come.

Types of Credit Card

There is more than one type of credit card available to examine, each one with its own specifications which are important to be aware of. When you are first looking for a card, you'll want to consider all of your options before settling down on one.

Standard Credit Card:

The standard credit card is the most commonly found type of credit card, it allows the user to carry a balance. The balance system on this type of card is known as a revolving balance: as credit spent on the card becomes available again as the balance is payed down. A finance charge will be placed on the balance matched with the standard credit card if the balance is carried from month to month. Payments on a standard card must be made by a specific due date. Should you fail to at least make a minimum payment you will be charged with a late payment charge.

Charge Card:

The charge card does not have a credit limit but the balance must be paid in full each month. These cards do not allow you to carry the balance and there is no option of minimum payment, there is only the one time full payment. Failure to make this payment can result in a fee, another penalty or even cancellation of the card itself.

Limited Purpose Card:

These are credit cards which can only be used at specific gas stations or certain stores like Macy’s to name one. They are used just like credit cards, placing a finance charge on a month to month balance, they allow for minimum payments and charge late fees.

Secured Credit Card:

Used primarily by people with poor credit histories or no prior credit history at all. Unlike most credit cards, you place a deposit of your own money to spend using the card. Instead of borrowing credit, you are spending a deposit of your own money. Depending on how much of the deposit limit you’ve used and your prior history you may be allowed to carry a revolving balance from month to month. They are good to use should you need to establish credit or attain good credit.

Prepaid Credit Card:

Similar to a Secured credit card, a prepaid card establishes credit via an amount you “load” onto the card. For example, if I place $4,000 on the card, then I can use that $4,000 until it is spent. As I use up my loaded balance, I can go back and reload the card with more money.

Standard Credit Card:

The standard credit card is the most commonly found type of credit card, it allows the user to carry a balance. The balance system on this type of card is known as a revolving balance: as credit spent on the card becomes available again as the balance is payed down. A finance charge will be placed on the balance matched with the standard credit card if the balance is carried from month to month. Payments on a standard card must be made by a specific due date. Should you fail to at least make a minimum payment you will be charged with a late payment charge.

Charge Card:

The charge card does not have a credit limit but the balance must be paid in full each month. These cards do not allow you to carry the balance and there is no option of minimum payment, there is only the one time full payment. Failure to make this payment can result in a fee, another penalty or even cancellation of the card itself.

Limited Purpose Card:

These are credit cards which can only be used at specific gas stations or certain stores like Macy’s to name one. They are used just like credit cards, placing a finance charge on a month to month balance, they allow for minimum payments and charge late fees.

Secured Credit Card:

Used primarily by people with poor credit histories or no prior credit history at all. Unlike most credit cards, you place a deposit of your own money to spend using the card. Instead of borrowing credit, you are spending a deposit of your own money. Depending on how much of the deposit limit you’ve used and your prior history you may be allowed to carry a revolving balance from month to month. They are good to use should you need to establish credit or attain good credit.

Prepaid Credit Card:

Similar to a Secured credit card, a prepaid card establishes credit via an amount you “load” onto the card. For example, if I place $4,000 on the card, then I can use that $4,000 until it is spent. As I use up my loaded balance, I can go back and reload the card with more money.

Credit Card Fees

Unfortunately very few things in this life are free. Credit Cards can bog you down with lots of different fees, some of which are specific to a certain type of card. Make sure you know what you are paying or will have to pay in the future when selecting a card. These are the types of fees you will encounter with a credit card:

Annual Fee:

Most commonly found with secured cards, charge cards, and premium cards such as gold and platinum cards with special rewards. This is the yearly fee you are charged simply for carrying the card.

Application Fee:

Relatively self-explanatory, it is a fee you are charged simply for applying for a credit card. Most cards do not have an application fee, you are more likely to find them on secured credit cards because there is a longer process in attaining them.

Finance Charge:

Interest applied on a balance that is carried from month to month beyond the given grace period. There are only two types of credit cards without a finance charge; Charge and Prepaid. As mentioned in the previous section a Charge card’s balance must be paid in full. A Prepaid credit card does not have a finance charge because you “load” your own money onto the card.

Balance Transfer Fee:

A fee charged when you transfer a balance from one credit card account into another. It is only charged when you transfer the balance and is paid in addition to the finance charge of carrying your balance from month to month. This is typically done by users who wish to move credit card debt to a card with a lower interest rate, fewer penalties, or various rewards. Another form of a balance transfer fee is a cash advance which allows card holders to withdraw a certain amount of cash whether from an ATM or at the bank. The interest rate on a cash advance is usually very high and accrues immediately. Balance Transfers are not always a good idea. In some instances they can cost you more interest than you were previously paying and can damage your credit score.

For Example:

Let’s say I’m carrying a balance of $3,500.

On my original account, I am paying an APR (interest rate) of 9%; 9% of $3,500 = 0.09 x 3500 = $315/year to carry that balance.

I find a new card that offers me an APR of 5.9%, a little over half of what I was paying before.

I decide to transfer my balance: 5.9% of $3,500 = .059 x 3500 = $206.50/year to carry the balance.

However, to transfer that balance, I pay a balance transfer fee of 4% of $3,500 - .04 x 3500 = $140 balance transfer fee.

So, at the end of the year I have paid: $140 transfer fee +$206.50 finance charge = $346.50 as opposed to my standard $315. The transfer fee is a one-time payment, but it is still another fee to pay.

Late Payment Fee:

A fee which is charged should the credit card holder fail to make a payment by the date it is due. In order to avoid a late payment fee you must at least make a minimum payment on your balance. Some companies will increase the fee with each violation. For example, first time violation may be $10, second violation may be $20, third time violation could be $30, etc. If you can’t make the full payment, at least make a minimum payment so as not to incur these fees.

Returned Check Fee:

This is only charged in instances where a check is used to pay for a balance. Should you pay for a balance with a check and the money in the checking account is not enough to cover the balance, you will be charged with a checking fee. Avoiding it is as easy as simply checking how much you have in your checking account and adding money should you have to before sending in the check.

Annual Fee:

Most commonly found with secured cards, charge cards, and premium cards such as gold and platinum cards with special rewards. This is the yearly fee you are charged simply for carrying the card.

Application Fee:

Relatively self-explanatory, it is a fee you are charged simply for applying for a credit card. Most cards do not have an application fee, you are more likely to find them on secured credit cards because there is a longer process in attaining them.

Finance Charge:

Interest applied on a balance that is carried from month to month beyond the given grace period. There are only two types of credit cards without a finance charge; Charge and Prepaid. As mentioned in the previous section a Charge card’s balance must be paid in full. A Prepaid credit card does not have a finance charge because you “load” your own money onto the card.

Balance Transfer Fee:

A fee charged when you transfer a balance from one credit card account into another. It is only charged when you transfer the balance and is paid in addition to the finance charge of carrying your balance from month to month. This is typically done by users who wish to move credit card debt to a card with a lower interest rate, fewer penalties, or various rewards. Another form of a balance transfer fee is a cash advance which allows card holders to withdraw a certain amount of cash whether from an ATM or at the bank. The interest rate on a cash advance is usually very high and accrues immediately. Balance Transfers are not always a good idea. In some instances they can cost you more interest than you were previously paying and can damage your credit score.

For Example:

Let’s say I’m carrying a balance of $3,500.

On my original account, I am paying an APR (interest rate) of 9%; 9% of $3,500 = 0.09 x 3500 = $315/year to carry that balance.

I find a new card that offers me an APR of 5.9%, a little over half of what I was paying before.

I decide to transfer my balance: 5.9% of $3,500 = .059 x 3500 = $206.50/year to carry the balance.

However, to transfer that balance, I pay a balance transfer fee of 4% of $3,500 - .04 x 3500 = $140 balance transfer fee.

So, at the end of the year I have paid: $140 transfer fee +$206.50 finance charge = $346.50 as opposed to my standard $315. The transfer fee is a one-time payment, but it is still another fee to pay.

Late Payment Fee:

A fee which is charged should the credit card holder fail to make a payment by the date it is due. In order to avoid a late payment fee you must at least make a minimum payment on your balance. Some companies will increase the fee with each violation. For example, first time violation may be $10, second violation may be $20, third time violation could be $30, etc. If you can’t make the full payment, at least make a minimum payment so as not to incur these fees.

Returned Check Fee:

This is only charged in instances where a check is used to pay for a balance. Should you pay for a balance with a check and the money in the checking account is not enough to cover the balance, you will be charged with a checking fee. Avoiding it is as easy as simply checking how much you have in your checking account and adding money should you have to before sending in the check.

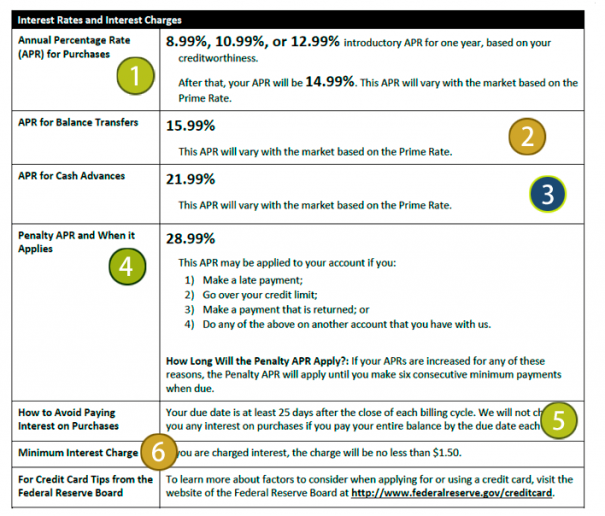

Schumer Box

A schumer box is a table contained within credit card marketing materials which details the costs associated with that credit card. In 1988 New York Senator Charles Schumer, a member of the House of Representatives introduced the Truth in Lending Act (TILA). The result of which was the Schumer Box which makes it easier for consumers like you to compare different credit card offers and determine how much the card will cost you. As a consumer, you should use this box to help you make an informed decision on which credit card to choose. Unless you know what you’re looking at, a Schumer Box can seem confusing. So, to make sure you’re prepared, here’s a handy guide to the information in a Schumer Box. Before we get into too much detail however, you need to know what APR is. Annual Percentage Rate (APR) is the annual rate charged for borrowing money. It is a measurement used to compare different loans. It considers interest rate, term, and fees to illustrate the total cost of credit. The lower the APR, the lower the cost of the loan. The APR works hand in hand with the finance charge of the card. The importance of the APR when selecting a card is based on how you think you will use the card. If you plan on paying off your entire balance in full, APR isn’t all that important to you because you won’t incur a finance charge. However, if you think you will be carrying your balance, the APR is extremely important to you. Being aware of the card’s APR and fees can save you thousands of dollars in years to come. This is where the Schumer Box comes in. Detailed below are all the parts of a Schumer Box, this is also where you will find the APR.

|

If you look at Section 1 on the image, you will see the introductory rate of the card. It lists how long the introductory rate lasts as well as the regular interest rate and whether it is a variable rate (changes regularly) or a fixed rate (won’t change at all). In this example, you may notice that they list 3 different introductory rates. If you have very good credit, your rate will be 8.99%, if it isn’t great it will be higher. After one year, the regular rate kicks in at 14.99%. Should you have a variable interest rate, there must be an explanation of how that rate is created. On many cards this generally means a Prime Rate plus a certain given amount determined on your credit.

Sections 2,3, and 4 on the image detail other types of interest rates (APR) on the card. These include cash advances, balance transfers, defaults, and penalties. You already know what the cash advance and balance transfer fees are. A default is the failure to pay interest or principal when it is due. A person may default when they cannot make a required payment or are unwilling to honor debt. The penalties rate is 28.99% and is incurred when the activities explained in the box occur. Section 5 of the image shows the grace period this particular card offers. In this example, the grace period is 25 days. Most cards will have a grace period of 20 or a maximum of 30 days. In the agreement you make when you sign up for the card, you are agreeing to pay back your credit in full by its due date. If you carry a balance, meaning you do not pay back what you owe in its entirety, you will not have access to your grace period. The image provides a clear explanation on how to avoid paying interest. Section 6 details the minimum amount of money you will be charged if you carry a balance. In this scenario that balance is $1.50. |

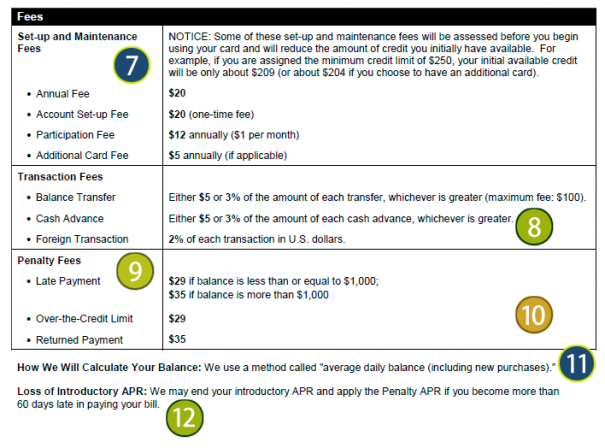

Section 7 details the annual fees you will be charged to have an active account. Not all credit cards have these fees, a “standard credit card” will not have these fees. I’ll describe the different types of cards later. Some rewards cards may charge between $35 and $75 a year, other premium cards may charge $95 to $450 a year. Cards with annual fees may waive the fees for your first year with the card. In the provided example, you can see that there is an annual fee, account set-up fee, participation fee, and additional card fee. The costs are listed for each as well as an explanation on how these fees can reduce available credit.

Section 8 describes any fees applicable for foreign purchases as well as other transaction fees. This scenario has a charge of 2%, most cards generally have a 3% charge. This percentage even includes purchases made in US dollars if made in another country. This box also includes other common fees such as balance transfer and cash advance fees, generally between 3% and 5% of the amount transferred. You can also see there is a minimum fee, if you transfer a smaller amount the card issuer still gets an amount of it.

Sections 9 and 10 detail various penalty fees. In this example the fees they have are late payment, over-the-credit limit, and returned payment. It is common to find late fees and over-the-limit fees around $35, though some companies will base it off of your credit card balance and the fee can range from $15 to $45.

Sections 11 and 12 detail exceptions and how interest is charged to your account. In this example, they use a method known as the “average daily balance” method. This means the sum of your balance on each day of the cycle is divided by the number of days in that billing cycle. Interest is charged each day, much to the advantage of the issuer of your card. In other Schumer Boxes you may find information further detailing variable rates or where the Prime Rate is published.

Section 8 describes any fees applicable for foreign purchases as well as other transaction fees. This scenario has a charge of 2%, most cards generally have a 3% charge. This percentage even includes purchases made in US dollars if made in another country. This box also includes other common fees such as balance transfer and cash advance fees, generally between 3% and 5% of the amount transferred. You can also see there is a minimum fee, if you transfer a smaller amount the card issuer still gets an amount of it.

Sections 9 and 10 detail various penalty fees. In this example the fees they have are late payment, over-the-credit limit, and returned payment. It is common to find late fees and over-the-limit fees around $35, though some companies will base it off of your credit card balance and the fee can range from $15 to $45.

Sections 11 and 12 detail exceptions and how interest is charged to your account. In this example, they use a method known as the “average daily balance” method. This means the sum of your balance on each day of the cycle is divided by the number of days in that billing cycle. Interest is charged each day, much to the advantage of the issuer of your card. In other Schumer Boxes you may find information further detailing variable rates or where the Prime Rate is published.

Rewards and Incentives

When it comes to choosing cards, companies will often entice the consumer with special rewards they will attain from using their card. When choosing a card, it is important to look for a reward system which you know you will use regularly. It is important to make the card work for you as much as possible. When looking at reward programs make sure to examine the fine print. A card may advertise that you will get 6% cash back, but limitations may be in place stating you can only receive that amount in certain categories which rotate throughout the year. Understand all of the redemption fees, blackout dates, and expiration policies which go hand in hand with your rewards.

Common Rewards/Incentives:

Cash Back

Common Rewards/Incentives:

Cash Back

- This reward offers an amount of cash back to you at the end of the year. This amount is usually a percentage based around how much you spent using the card. For example, let’s say my cash back is 2% and I spent $15,000 in a single calendar year I earn back $300. This cash back is usually in the form of a check or a gift card. In some cases the company will offer the user to use their cash back as credit on their next statement.

- This reward commonly gives the card holder one mile for each dollar spent on the card. These miles are accumulated over time and can be used to buy an airline ticket. Most airlines will have seats reserved for rewards promotions, but they can only be accessed if you have the needed amount of points to receive a free airline ticket. It is important to familiarize yourself with the requirements of specific programs before you chose it. This particular reward won’t be useful to you if you rarely travel so it isn’t something you’d choose.

Avoiding Marketing Schemes

The 0% APR Trap

In order to entice new customers, credit card companies flaunt advertisements flaunting a 0% APR on interest and balance transfers. This however is often a trap. Balance Transfers come with a fee of their own, so while there may be a 0% APR, the individual fee may be incredibly hard so make sure to do the math calculating how much you’re spending. These low APR rates are often referred to as “teaser rates”, meaning they will only last for a short period of time. Once this introductory rate period is over, the regular rate usually increases drastically to a percentage much higher than you want to pay, or were paying previously on a different card. If you happen to be late on a payment or go over your credit limit during this introductory period, you may be subject to losing that special 0% APR rate and forced to deal with the higher interest rates. When picking a card look for longer introductory periods, but be sure to see what is covered in that period. It can also hurt your credit score because every time you apply for a new card, the company requests a credit report to determine your credit worthiness. If you have many requests for a credit report, you are seen as a greater risk. Your score will drop depending on how good it was to begin with. If you have a strong credit score, it may only drop a few points. If you have a poor credit score it can be a much bigger hit.

Independent Marketers

These are companies you’ll want to avoid when selecting a credit card. These are easy to avoid but you should remain aware of them. Generally, offers from independent marketers will come in plain envelopes without a bank or brand logo. Rather, they may be stamped with more generic terms like “Credit Card Administration”. Many of these offers will attempt to charge application fees or various other fees.

In order to entice new customers, credit card companies flaunt advertisements flaunting a 0% APR on interest and balance transfers. This however is often a trap. Balance Transfers come with a fee of their own, so while there may be a 0% APR, the individual fee may be incredibly hard so make sure to do the math calculating how much you’re spending. These low APR rates are often referred to as “teaser rates”, meaning they will only last for a short period of time. Once this introductory rate period is over, the regular rate usually increases drastically to a percentage much higher than you want to pay, or were paying previously on a different card. If you happen to be late on a payment or go over your credit limit during this introductory period, you may be subject to losing that special 0% APR rate and forced to deal with the higher interest rates. When picking a card look for longer introductory periods, but be sure to see what is covered in that period. It can also hurt your credit score because every time you apply for a new card, the company requests a credit report to determine your credit worthiness. If you have many requests for a credit report, you are seen as a greater risk. Your score will drop depending on how good it was to begin with. If you have a strong credit score, it may only drop a few points. If you have a poor credit score it can be a much bigger hit.

Independent Marketers

These are companies you’ll want to avoid when selecting a credit card. These are easy to avoid but you should remain aware of them. Generally, offers from independent marketers will come in plain envelopes without a bank or brand logo. Rather, they may be stamped with more generic terms like “Credit Card Administration”. Many of these offers will attempt to charge application fees or various other fees.