Credit Card Statement

So, you've spent all that money buying things with your brand new credit card! YAY!! Now it's time to pay back what you ow from all of those purchases you made. Hopefully you didn't go on a massive shopping spree because you're gonna owe a lot if you did! Your bank or whatever financial institution you're partnered with will send you a credit card statement in the mail, or sometimes online should you choose that option. A credit card statement is a written record compiled by your financial institution which lists all transactions for a credit card account including deposits, withdrawals, checks, electronic transfers, fees, various other charges, and interest. AKA billing statement. It's a fairly simple document if you know what to look for etc. It's important to look it over to check for any purchases or actions which you don't recognize or never made. Receiving the credit card statement kicks off your grace period. The statement will tell you what balance you owe, and when you must pay that balance by. Should you make any purchases between receiving this document, and paying the balance listed, you will not be charged interest.

Here's a handy little guide of a sample statement:

Here's a handy little guide of a sample statement:

|

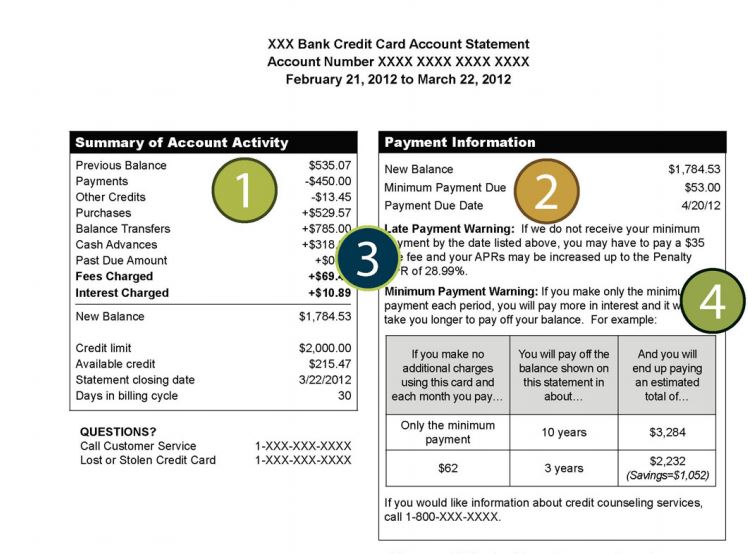

Section 1: Account Summary

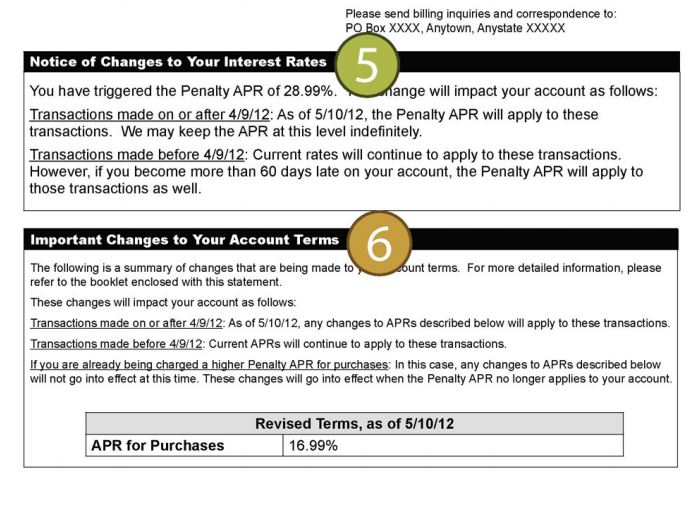

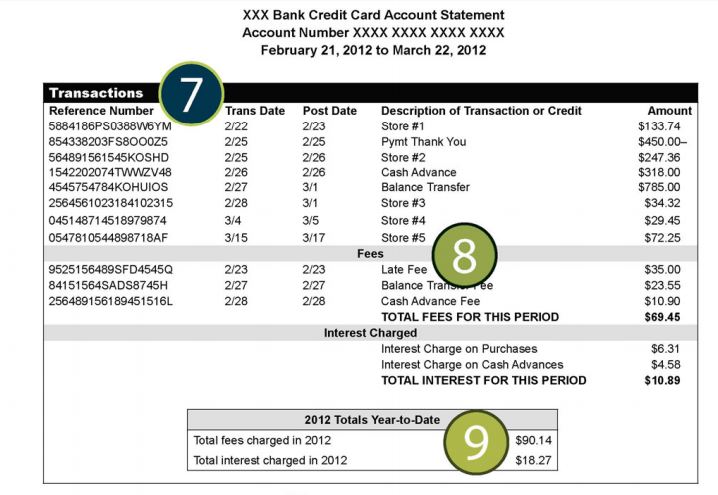

This is a summary of all the activity on your account including payments, credits, purchases, balance transfers, cash advances, fees, interest, and past dues. This section will also include your new balance, any available credit you have left, and the last day of your billing cycle. Any payments or charges after this day will show up on the next bill. Section 2: Payment Information This section details your new balance, the minimum payment you must make, and the date it is due by. Payments are considered on time if they are made by 5 p.m. on the day they are due. Should the due date be a weekend or a holiday and you mail in your bill, the payment is accepted by 5 p.m. the following business day. Section 3: Late Payment Notice This section details the fees you will be charged with should the payment due be late. Section 4: Minimum Payment Notice A useful bit which estimates how long it will take you to pay off your balance should you only make the minimum payment. It also includes an estimate of how much you will pay in order to pay off your bill in three ears with interest and assuming there are no additional charges. Section 5: Interest Rate Changes This notifies you should there be any changes to the interest rate which is applied to your account. For example, should you trigger a penalty rate by going over your credit limit, this section will notify you of your new interest rate. You must be notified at least 45 days before the changes are applied. Section 6: Other Account Changes Should your credit card company be planning on making any changes to your account or new information concerning interest rates, that information will be provided here. Like with the information in the previous section, you must be notified at least 45 days prior to changes. Section 7: Transaction History This is a list of all transactions which have occurred since you received your last statement. This may include purchases, payments, credits, cash advances, and balance transfers. Depending on your credit card company, the statement have have these transactions categorized by type, date, or user (if there are multiple users on the account). This is the section you should check for any unauthorized transactions or other various problems. Section 8: Fees and Interest Charges This lists all the fees and interest rates which apply to different aspects of your account separately from your bill. Different interest rates apply to different actions such as purchases or cash advances. Credit Card companies are required by law to include this information. Section 9: Year-to-Date Total This details the total amount of money you have paid in fees and interest rates within the past year. Many of these fees can be avoided by paying your bill on time, in full, and by not over charging on your card. |

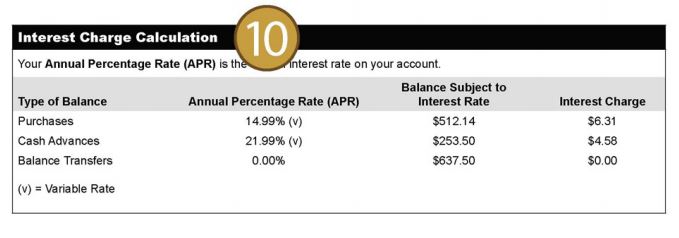

Section 10: Interest Charge Calculation

Summary of each interest rate on the various types of transactions such as account balances. It includes the amount of each account and the interest rate applied to each type of transaction.

Summary of each interest rate on the various types of transactions such as account balances. It includes the amount of each account and the interest rate applied to each type of transaction.

Reducing and Avoiding Interest Rates

Here is where the finance charge and APR are huge, I’m also going to be tying in vocabulary from the “Basics of Credit” section, just in case you’ve forgotten the definitions here's a link to the glossary. As a mentioned in the “Schumer Box” section, the finance charge and APR go hand in hand; if you plan on carrying your balance you want a card with a lower APR. Things are going to get tricky from this point on so before getting into too much detail, let’s look at an example of APR and its impact:

Card A has an APR of 8.9%; Card B has an APR of 15.9%

Let’s assume that I carry a balance on my card of $1,000,

Card A: annual interest cost of 8.9% of $1,000 = 0.089 x 1000 = $89/year

Card B: annual interest cost of 15.9% of $1,000 = 0.159 x 1000 = $159/year

This example doesn’t factor in minimum payments or anything else, it’s just to show you how important the APR is when factoring interest into credit card choice. If you notice, with Card B you’re spending an additional $70 which is not beneficial to you in the slightest, it’s a waste. You’re paying more money than if you payed off the entirety of the $1,000 balance. Once you begin to carry a balance, the finance charge kicks in. Interest will begin to accumulate on your balance and purchases, leading you into debt.

A typical minimum payment is usually 1% to 2% of your balance or $15, which ever turns out to be more money. Going back to the same numbers from above, let's calculate what the minimum payment of the $1,000 balance would be if my card as a minimum payment of 3% on Card A and 2% on Card B and my grace period is over, meaning the interest from above applies.

Card A: APR 8.9% - 0.089 x 1000 = $89

89/12 = $7.42 Monthly Interest

1000 + 7.42 = 1,007.42 Total Balance

0.03 x 1007.42 = $30.22 Minimum Payment

Card B: APR 15.9% - 0.159 x 1000 = $159

159/12 = $13.25 Monthly Interest

1000 + 13.25 = $1,013.25 Total Balance

0.02 x 1013.25 = $20.27 Minimum Payment

Now that we’ve looked at APR and minimum payments, let’s combine it with making credit card payments; we’ll look at it through a billing cycle. For the sake of this example, let’s say the billing cycle ends on the first day of the month, and my grace period is 20 days from my billing date. This means that my credit card payment is due the 21st of the month. I’ve run up a balance of $1,000 by my billing date and I am sent my statement. During the period between my receiving the bill (first day of the month) to when I must pay my bill (21st day of the month) I will not have to pay any finance charges on my balance or on any purchases I make in that period. If I pay my full $1,000 bill by the 21st, I will not suffer finance charges on that $1,000 or any purchases I made during the grace period.

Here’s an example:

Month: April

4/1: I receive my bill of $1,000; I need to pay this bill by 4/21

4/1 – 4/20: I spend $500, making my credit card balance $1,500. (Grace Period)

4/21: I pay the amount of $1,000 as stated on my bill; I do not suffer any finance charges.

Why? – My bill stated I needed to pay $1,000 by 4/21, any additional charges I make in between receiving the bill, and paying it off will not be charged any interest. My balance technically still has $500, but my bill stated I need to pay $1,000 by the payment date. What happens to that $500? For the sake of the example, let’s pretend I don’t make any other credit card purchases until my next billing cycle:

Month: May

5/1: I receive my bill of $500 – this is the amount I charged to my credit card during the grace period of the previous month. If I make purchases after my grace period is over I still will not incur finance charges, because I paid my bill during the grace period.

This whole process I described is paying your bill in full, you won’t be paying any interest and you are considered a deadbeat by the credit card company. They aren’t making any money off you. This is the most ideal scenario when using a credit card. Pay your bill in full by the date it is due and you’ll never have to worry about interest rates.

Now, let’s say times are tough and you can’t make the full payment, so you make a minimum payment or an amount less than the $1,000 in the bill. Finance charges will begin to accumulate on the balance of your card plus any additional purchases you make after the payment due date. Until you pay off your entire outstanding balance by the payment due date, you will lose your grace period.

Let’s look at a new example assuming you don’t make the full payment during the grace period. Remember, most credit cards have a credit limit so we will factor this into the example.

It’s a new year and you have just received a credit card with an APR of 10% and a Credit Limit of $3,000.

January:

You Spend: $2,500

Current Balance: $2,500

February:

Minimum Payment: $500 (Your line of credit is now $1,000)

Current Balance: $2,000

You Spend: $800

At the end of the month your balance will be:

[ (previous month balance + money spent) + APR]

[ (2,000 + 800) + 10%]

[ 2,800 + 10%] – Before adding the 10% you need to calculate what 10% of 2,800 is: (2800 x .10) = 280

2,800 + 280 = 3,080

New Balance: $3,080

March:

Balance: $3,080 (Your line of credit is $200)

Notice over the course of the 3 months how much the line of credit has reduced. By march, you can only spend $200 worth on your credit card. If you continue to make purchases and make only minimum payments this will lead you into a never-ending cycle of debt. If you are unable to make full payments the only way to end this cycle of debt is to make minimum payments without making any new purchases on the card.

The best way to avoid interest rates and falling into debt is to follow two simple rules: 1. Never charge more than you can pay back, and 2. pay back your balance in full. If you are forced to make a minimum payment, try not to use the credit card to purchase goods or services.

Card A has an APR of 8.9%; Card B has an APR of 15.9%

Let’s assume that I carry a balance on my card of $1,000,

Card A: annual interest cost of 8.9% of $1,000 = 0.089 x 1000 = $89/year

Card B: annual interest cost of 15.9% of $1,000 = 0.159 x 1000 = $159/year

This example doesn’t factor in minimum payments or anything else, it’s just to show you how important the APR is when factoring interest into credit card choice. If you notice, with Card B you’re spending an additional $70 which is not beneficial to you in the slightest, it’s a waste. You’re paying more money than if you payed off the entirety of the $1,000 balance. Once you begin to carry a balance, the finance charge kicks in. Interest will begin to accumulate on your balance and purchases, leading you into debt.

A typical minimum payment is usually 1% to 2% of your balance or $15, which ever turns out to be more money. Going back to the same numbers from above, let's calculate what the minimum payment of the $1,000 balance would be if my card as a minimum payment of 3% on Card A and 2% on Card B and my grace period is over, meaning the interest from above applies.

Card A: APR 8.9% - 0.089 x 1000 = $89

89/12 = $7.42 Monthly Interest

1000 + 7.42 = 1,007.42 Total Balance

0.03 x 1007.42 = $30.22 Minimum Payment

Card B: APR 15.9% - 0.159 x 1000 = $159

159/12 = $13.25 Monthly Interest

1000 + 13.25 = $1,013.25 Total Balance

0.02 x 1013.25 = $20.27 Minimum Payment

Now that we’ve looked at APR and minimum payments, let’s combine it with making credit card payments; we’ll look at it through a billing cycle. For the sake of this example, let’s say the billing cycle ends on the first day of the month, and my grace period is 20 days from my billing date. This means that my credit card payment is due the 21st of the month. I’ve run up a balance of $1,000 by my billing date and I am sent my statement. During the period between my receiving the bill (first day of the month) to when I must pay my bill (21st day of the month) I will not have to pay any finance charges on my balance or on any purchases I make in that period. If I pay my full $1,000 bill by the 21st, I will not suffer finance charges on that $1,000 or any purchases I made during the grace period.

Here’s an example:

Month: April

4/1: I receive my bill of $1,000; I need to pay this bill by 4/21

4/1 – 4/20: I spend $500, making my credit card balance $1,500. (Grace Period)

4/21: I pay the amount of $1,000 as stated on my bill; I do not suffer any finance charges.

Why? – My bill stated I needed to pay $1,000 by 4/21, any additional charges I make in between receiving the bill, and paying it off will not be charged any interest. My balance technically still has $500, but my bill stated I need to pay $1,000 by the payment date. What happens to that $500? For the sake of the example, let’s pretend I don’t make any other credit card purchases until my next billing cycle:

Month: May

5/1: I receive my bill of $500 – this is the amount I charged to my credit card during the grace period of the previous month. If I make purchases after my grace period is over I still will not incur finance charges, because I paid my bill during the grace period.

This whole process I described is paying your bill in full, you won’t be paying any interest and you are considered a deadbeat by the credit card company. They aren’t making any money off you. This is the most ideal scenario when using a credit card. Pay your bill in full by the date it is due and you’ll never have to worry about interest rates.

Now, let’s say times are tough and you can’t make the full payment, so you make a minimum payment or an amount less than the $1,000 in the bill. Finance charges will begin to accumulate on the balance of your card plus any additional purchases you make after the payment due date. Until you pay off your entire outstanding balance by the payment due date, you will lose your grace period.

Let’s look at a new example assuming you don’t make the full payment during the grace period. Remember, most credit cards have a credit limit so we will factor this into the example.

It’s a new year and you have just received a credit card with an APR of 10% and a Credit Limit of $3,000.

January:

You Spend: $2,500

Current Balance: $2,500

February:

Minimum Payment: $500 (Your line of credit is now $1,000)

Current Balance: $2,000

You Spend: $800

At the end of the month your balance will be:

[ (previous month balance + money spent) + APR]

[ (2,000 + 800) + 10%]

[ 2,800 + 10%] – Before adding the 10% you need to calculate what 10% of 2,800 is: (2800 x .10) = 280

2,800 + 280 = 3,080

New Balance: $3,080

March:

Balance: $3,080 (Your line of credit is $200)

Notice over the course of the 3 months how much the line of credit has reduced. By march, you can only spend $200 worth on your credit card. If you continue to make purchases and make only minimum payments this will lead you into a never-ending cycle of debt. If you are unable to make full payments the only way to end this cycle of debt is to make minimum payments without making any new purchases on the card.

The best way to avoid interest rates and falling into debt is to follow two simple rules: 1. Never charge more than you can pay back, and 2. pay back your balance in full. If you are forced to make a minimum payment, try not to use the credit card to purchase goods or services.