What is a Credit Report?

A Credit Report is a report issued by an independent credit agency that contains information concerning a loan applicant’s credit history and current credit standing. It is important to look at your credit report at least once a year to review it for any errors or mistakes. You definitely want to look at it before making large purchases such as a home and a car. You’re not the only person who can see your credit report. In fact, when you fill out applications for credit cards, or seek to rent an apartments others are allowed to look at your report. Lenders will want to determine whether or not you’re worth the risk to lend credit; a landlord wants to make sure they can rely on you to pay the rent.

Now you know what it is and how it’s used, let’s take a look at its different parts.

Now you know what it is and how it’s used, let’s take a look at its different parts.

Components of a Credit Report

|

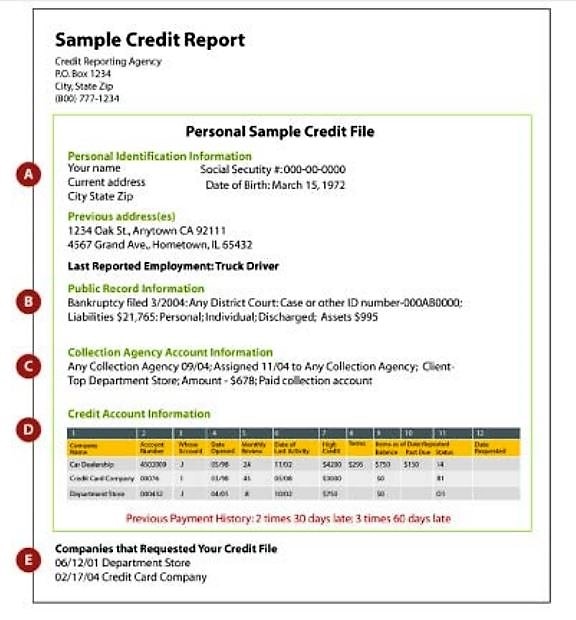

Section A: This portion contains personal information about you. This includes your Name, Social Security Number, date of birth, and various other forms of identification. On your credit report your social security number will look something like this: XX-XX-1234 – it is partially masked for your protection.

Section B: Contains Public Record Information. Here you will find any information listed about you in local, state, or federal court records. In this particular example, you have a bankruptcy filed. Section C: Collection Agency account information is included in this section. This is a company which specializes in collecting money to pay off your debts. Should you fail to pay back a creditor, a collection agency may be hired to get in touch with you. Section D: This section shows your credit history, including all of the places you have credit or have used credit. It is divided into 12 different columns. Section E: This final section is known as Inquiries. It lists all companies that have requested a copy of your credit report. Some credit reports may have this information in a different format or order from this particular example, but all credit reports will contain the information listed above. Credit reports may look different depending on where you get it. Though they might look different, they've got the same information. For an interactive credit report example, click here. For an example which looks at each piece of a credit report in more detail click here. |

Attaining a Credit Report

Attaining a copy of your credit report is easy, and the best part, it’s free! There is one minor exception to that free rule, you can only get your credit report for free once a year. During your life, however, you should only need to look at your credit report once a year.

So, now you’ve got it, great! What do you do with it? Reviewing your credit report is very much like reading over the first draft of a paper you write. You are looking for any mistakes within the report. These can range from relatively minor such as a misspelled name, or old address, to the more serious such as the wrong digits in your social security number, accounts you never opened and other errors in your credit history. This is why it’s important to save all of your receipts from purchases, know what you’ve spent and when so that you know when there is a mistake. If you do find a mistake, contact your lender and credit bureau immediately. More information on reviewing your credit card is in the next section!

- In the United States there are three major credit bureaus: Equifax, Experian, and Transunion. It is from them that you can get a copy of your credit report.

- According to the Fair Credit Reporting Act you are allowed to receive your credit report once a year free of charge from each of these three companies.

- You can easily access your credit report online at www.annualcreditreport.com which is run jointly by Equifax, Experian, and TransUnion. Follow the directions on the site and hey presto, you’ve got your credit report. You’ll be able to attain one from each group, which is a good idea so you can compare them.

- There are many other websites which advertise attaining a free credit report, use extreme caution around these sites as they will more than likely charge some form of a fee.

So, now you’ve got it, great! What do you do with it? Reviewing your credit report is very much like reading over the first draft of a paper you write. You are looking for any mistakes within the report. These can range from relatively minor such as a misspelled name, or old address, to the more serious such as the wrong digits in your social security number, accounts you never opened and other errors in your credit history. This is why it’s important to save all of your receipts from purchases, know what you’ve spent and when so that you know when there is a mistake. If you do find a mistake, contact your lender and credit bureau immediately. More information on reviewing your credit card is in the next section!

Reviewing a Report and How to Dispute Errors

It is important to remember that mistakes can happen on these reports. If you do find a mistake, don’t lose your head. It is now up to you to notify your lender or credit bureau, they won’t fix anything unless you tell them to.

When reviewing the report, make sure you are aware of the information you will find there. Know what you are looking at and from there you will be able to determine if there is an error or a problem. Let’s say you request your credit report and you get one from each of the three major bureaus: Equifax, Experian, and TransUnion and only the TransUnion report has an error. In this scenario, you would contact that credit bureau. If all three have an error, you must contact each one individually.

So, you’ve found something, what do you do now? Well, first, remain calm there are a series of simple steps you can follow. You’ll need to file a dispute with the credit bureau. Here are some things to keep in mind when you do this:

Snail Mail vs. Online: Filling out forms online has become a relatively normal aspect of life; it’s quick and it’s easy. Credit Bureaus will even allow you to upload any documents you have to help back up your dispute. However, the draw back to online is the online form is somewhat rigid and structured, plus there may be some legal language in the online form you’re not too sure about and don’t want to get involved with. The easiest option may in fact be snail mail, it’s a bit slower, but you’ve got less restrictions and you don’t have to worry about anything unsafe on the website. When you do mail it, be sure to check the credit bureau’s website for their address and any additional instructions they may have for mailing disputes. Take it to the post office and request a return receipt so you know when it is delivered.

The Right Form & What to Say: This is another example as to why snail mail is easier. When disputing your credit report, you can write a letter detailing each dispute you have and why you want it changed. Including a copy of your report with these areas highlighted or circled is also helpful. Make sure you are extremely clear when explaining the problem. Stick to facts and describe what is wrong, and why it is wrong. Pretend the person reading this dispute knows nothing about you. If there is more than one item in dispute, include a list. Make it specific, clear, and easy to follow. You may be asked to include supporting documentation when disputing a problem on your report. Make sure to look for any documents which will defend your claim whether it be payment records, court documents, identification, anything at all. When sending in these documents, never send the original, always make a copy. A good practice to make instances like these easier is to keep detailed and organized records. A well put together filing cabinet of all your original documents makes for an easy search instead of a wild panicky goose chase.

To make things even easier for you, the Federal Trade Commission (FTC) has a sample letter you can model on their website. Check it out here.

Keep yourself covered: Record everything involved in the process of disputing your credit report. Make copies of your dispute, record conversations you have with credit bureaus, banks, or your lender. Should you take legal action, it creates a hard copy paper trail to use.

Schedule: Be aware that it takes time for the credit bureau to receive and examine your claim. It can take up to 45 days for them to respond so be sure to notify the bureau as soon as possible when you find a dispute. If you’re about to make a large payment such as a student loan you don’t want to submit a dispute the day before. Plan in advance and be aware of large purchases you need to make in the future. A credit bureau shouldn’t take that long to get back to you, just be aware that it can take time.

Results: Following however long it takes, you’ll hear back from the credit bureau and their response will let you know if they have fixed whatever dispute you may have. The response you receive depends on whether or not your bank lender agrees with your claim. The credit bureau will send everything you sent them on to the bank and whatever they say following reviewing it goes. The credit bureau will ask whether or not they agree or disagree with the changes you want made. For example, let’s say there’s an account on your report you don’t recognize, so you dispute it. If they agree with you, it will be deleted from your record. Should the bank or lender disagree it will remain on the report.

Let’s say the bank or lender disagrees with your claim, or you’re having other trouble what then? Well, you’ve got a few options:

Try Again: You can file as many disputes about your credit report as you wish. If you feel that maybe you were missing important documentation, re-send the dispute with this added information. A word of caution however, if you continuously badger the lender and credit bureau with the same dispute over and over, they can determine your complaint to be “frivolous” and ignore you.

Account Mix-Up: Let’s say you file a dispute concerning accounts or debts that are not yours. A possible reason for this is your file has been mixed up with another person’s due to a similar name, address, or social security number. This is not a problem the lender or bank can solve as it comes from the credit bureau. Mistakes can happen when the bureau’s automation machine is trying to match millions of different pieces of information. Even if it gets cleared up, a similar problem could pop up in the future. An alternative and much less ideal reason for this problem is identity theft. Should you suspect identity theft, contact the bureau as soon as possible and put a fraud alert on your file so as to limit damage.

Alternative Actions: Let’s say for whatever reason you want to address it by a different means than sending a dispute to the bureau. Alternatively, you can send a dispute directly to your lender or bank where the information mix up first occurred.Should you choose this route, once again, the FTC's got you covered and they have a letter model for you to follow as it is different from the letter to the credit bureau. You can check it out here.

You should send this dispute the same way you would send it to the credit bureau. There is a slightly different letter writing format, for which the FTC has kindly provided a sample. Be sure to include all the same information you would have sent in the dispute to the credit bureau. If they agree with your dispute, be sure to send a correction to the credit bureau. It is highly recommended you start with a dispute to the credit bureau and it is a pre-requisite should you wish to take the issue to court.

If you feel the credit bureau isn’t getting the job done, you can file a complaint with the Consumer Financial Protection Bureau (CFPB). Credit bureaus work under the regulation of the CFPB and will have to respond to both your dispute, and to the CFPB. It may even make the credit bureau get back to you a bit faster.

Legal Action: This is the worst of the worst type scenario. If you feel there is a problem which the credit bureau isn’t solving, you can hire a lawyer who specializes in the Fair Credit Reporting Act to sue the credit bureau. This option is quite costly so be sure to consider all of your options and the impacts this can have. Consider the impact which mistakes on your report have had on your ability to attain a job, mortgage, or credit. If you don’t plan on applying for something like a loan or credit any time soon, the bad information on your report comes off after seven years.

When reviewing the report, make sure you are aware of the information you will find there. Know what you are looking at and from there you will be able to determine if there is an error or a problem. Let’s say you request your credit report and you get one from each of the three major bureaus: Equifax, Experian, and TransUnion and only the TransUnion report has an error. In this scenario, you would contact that credit bureau. If all three have an error, you must contact each one individually.

So, you’ve found something, what do you do now? Well, first, remain calm there are a series of simple steps you can follow. You’ll need to file a dispute with the credit bureau. Here are some things to keep in mind when you do this:

Snail Mail vs. Online: Filling out forms online has become a relatively normal aspect of life; it’s quick and it’s easy. Credit Bureaus will even allow you to upload any documents you have to help back up your dispute. However, the draw back to online is the online form is somewhat rigid and structured, plus there may be some legal language in the online form you’re not too sure about and don’t want to get involved with. The easiest option may in fact be snail mail, it’s a bit slower, but you’ve got less restrictions and you don’t have to worry about anything unsafe on the website. When you do mail it, be sure to check the credit bureau’s website for their address and any additional instructions they may have for mailing disputes. Take it to the post office and request a return receipt so you know when it is delivered.

The Right Form & What to Say: This is another example as to why snail mail is easier. When disputing your credit report, you can write a letter detailing each dispute you have and why you want it changed. Including a copy of your report with these areas highlighted or circled is also helpful. Make sure you are extremely clear when explaining the problem. Stick to facts and describe what is wrong, and why it is wrong. Pretend the person reading this dispute knows nothing about you. If there is more than one item in dispute, include a list. Make it specific, clear, and easy to follow. You may be asked to include supporting documentation when disputing a problem on your report. Make sure to look for any documents which will defend your claim whether it be payment records, court documents, identification, anything at all. When sending in these documents, never send the original, always make a copy. A good practice to make instances like these easier is to keep detailed and organized records. A well put together filing cabinet of all your original documents makes for an easy search instead of a wild panicky goose chase.

To make things even easier for you, the Federal Trade Commission (FTC) has a sample letter you can model on their website. Check it out here.

Keep yourself covered: Record everything involved in the process of disputing your credit report. Make copies of your dispute, record conversations you have with credit bureaus, banks, or your lender. Should you take legal action, it creates a hard copy paper trail to use.

Schedule: Be aware that it takes time for the credit bureau to receive and examine your claim. It can take up to 45 days for them to respond so be sure to notify the bureau as soon as possible when you find a dispute. If you’re about to make a large payment such as a student loan you don’t want to submit a dispute the day before. Plan in advance and be aware of large purchases you need to make in the future. A credit bureau shouldn’t take that long to get back to you, just be aware that it can take time.

Results: Following however long it takes, you’ll hear back from the credit bureau and their response will let you know if they have fixed whatever dispute you may have. The response you receive depends on whether or not your bank lender agrees with your claim. The credit bureau will send everything you sent them on to the bank and whatever they say following reviewing it goes. The credit bureau will ask whether or not they agree or disagree with the changes you want made. For example, let’s say there’s an account on your report you don’t recognize, so you dispute it. If they agree with you, it will be deleted from your record. Should the bank or lender disagree it will remain on the report.

Let’s say the bank or lender disagrees with your claim, or you’re having other trouble what then? Well, you’ve got a few options:

Try Again: You can file as many disputes about your credit report as you wish. If you feel that maybe you were missing important documentation, re-send the dispute with this added information. A word of caution however, if you continuously badger the lender and credit bureau with the same dispute over and over, they can determine your complaint to be “frivolous” and ignore you.

Account Mix-Up: Let’s say you file a dispute concerning accounts or debts that are not yours. A possible reason for this is your file has been mixed up with another person’s due to a similar name, address, or social security number. This is not a problem the lender or bank can solve as it comes from the credit bureau. Mistakes can happen when the bureau’s automation machine is trying to match millions of different pieces of information. Even if it gets cleared up, a similar problem could pop up in the future. An alternative and much less ideal reason for this problem is identity theft. Should you suspect identity theft, contact the bureau as soon as possible and put a fraud alert on your file so as to limit damage.

Alternative Actions: Let’s say for whatever reason you want to address it by a different means than sending a dispute to the bureau. Alternatively, you can send a dispute directly to your lender or bank where the information mix up first occurred.Should you choose this route, once again, the FTC's got you covered and they have a letter model for you to follow as it is different from the letter to the credit bureau. You can check it out here.

You should send this dispute the same way you would send it to the credit bureau. There is a slightly different letter writing format, for which the FTC has kindly provided a sample. Be sure to include all the same information you would have sent in the dispute to the credit bureau. If they agree with your dispute, be sure to send a correction to the credit bureau. It is highly recommended you start with a dispute to the credit bureau and it is a pre-requisite should you wish to take the issue to court.

If you feel the credit bureau isn’t getting the job done, you can file a complaint with the Consumer Financial Protection Bureau (CFPB). Credit bureaus work under the regulation of the CFPB and will have to respond to both your dispute, and to the CFPB. It may even make the credit bureau get back to you a bit faster.

Legal Action: This is the worst of the worst type scenario. If you feel there is a problem which the credit bureau isn’t solving, you can hire a lawyer who specializes in the Fair Credit Reporting Act to sue the credit bureau. This option is quite costly so be sure to consider all of your options and the impacts this can have. Consider the impact which mistakes on your report have had on your ability to attain a job, mortgage, or credit. If you don’t plan on applying for something like a loan or credit any time soon, the bad information on your report comes off after seven years.