What is a Credit Score?

A credit score is a numerical value which determines an individual's creditworthiness based off of 5 criteria.

How Credit Score is Determined

Your credit score is very similar to the honor/dishonor system found in the game "Red Dead Redemption". You gained honor points for good deeds, and became less honorable for bad deeds. The difference between the game and credit scores is you're not going on adventures in the wild west. You gain points for good credit behavior, and lose points for bad credit behavior. Your credit score is also known as your FICO Score, so named after the Fair Isaac Corporation which created the formula for determining credit score. Your credit score generally ranges from 300-850, the higher your score, the better. The score itself is based on a mathematical equation credit lenders use to determine whether or not you are worth the risk to lend money to. If you have a higher credit score, it generally means you are financially responsible and a very low risk. A lower credit score suggests you are not financially responsible, and the lender is much less likely to take the risk and lend you money. It makes sense, if you lend your friend some cash and they always pay you back, you’re more likely to lend them cash in the future. If you lend your friend cash and they never pay you back, you won’t be lending them anymore money in the future.

Here's a handy dandy little chart:

Here's a handy dandy little chart:

Components of a Credit Score

There are five components which make up your credit score. Each of the five elements are important, but some hold more weight than others. The 5 components are: Payment History (35%), Amount of Debt (30%), Length of Credit History (15%), New Credit (10%), and Credit Type Mix (10%).

1. Payment History (35%):

How well you have paid back all of your past debt is the most important factor in determining your credit score. Lenders will look towards your past behavior to determine what your future behavior will look like. If you make all your payments on time and have no missed payments, then you won’t have a problem. Missing payments or being late on payments will hurt your credit score. There is some distinction to be made here. If, for example, you have late payments in your recent credit history, the lender will assume you are experiencing hardships and probably won’t want to risk lending you the money. If, however, you made late payments a few years ago and have had a strong history since then, they will assume you’ve gotten over hard times and are probably worth the risk. Simply put, best way to ensure this component stays high is to make your payments on any outstanding debt timely and consistent.

2. Amount of Debt (30%):

This category is where credit cards play a large role. Remember, credit cards are revolving lines of credit, meaning if my credit limit is $3,000 and I borrow $1,000 then pay back that $1,000 my credit limit is restored to its full $3,000 and the cycle continues. This type of credit is weighed very heavily when lenders look at the amount of debt you have compared to your limit. For example, if a lender sees that your limit is $3,000 and every month you max out that limit, they’re going to assume you’re not financially responsible. The best way to protect your credit score in this category is to keep a low credit card balance in regards to your limit. You should never borrow more than 50% of your credit limit on a single card. The ideal spending percent is about 30% of your credit limit. If you have multiple cards, it is better to owe smaller amounts on these cards, than to have a single card which is continuously maxed out.

3. Length of Credit History (15%):

This is the length of time any credit accounts you own have been open and in use. The longer your credit history, the easier it is for a lender to determine whether or not you are worth the risk. Someone who is just starting out in developing credit will not have a perfect credit score simply because you have not been using credit long enough. Credit cards are also not the only sources of credit and usually people with excellent credit scores have at least three sources of credit such as credit cards or installments loans. They are also usually on time with their payments and have had a credit history for at least seven years. When you start out using credit, usually with a credit card, make sure to be responsible and always pay your balance on time and in full. As you begin to accumulate more credit, it is better to keep and use old credit accounts because they have a longer and more detailed history for lenders to examine. Don’t close the account, keep it open and use it often enough to keep it active.

4. New Credit (10%):

Be cautious when opening new credit accounts. Opening too many credit accounts at the same time will make lenders assume you are experiencing hard times financially. You should only request and take on new credit when you really need it or when it makes financial sense.

5. Credit Type Mix (10%):

As mentioned in credit history, someone with an excellent credit score has more than one form of credit. This is made up of their revolving credit, credit card, and their installment credit, car and mortgage loans. Having a mix of credit sources signals to the lender that you can handle the responsibility of multiple forms of credit.

1. Payment History (35%):

How well you have paid back all of your past debt is the most important factor in determining your credit score. Lenders will look towards your past behavior to determine what your future behavior will look like. If you make all your payments on time and have no missed payments, then you won’t have a problem. Missing payments or being late on payments will hurt your credit score. There is some distinction to be made here. If, for example, you have late payments in your recent credit history, the lender will assume you are experiencing hardships and probably won’t want to risk lending you the money. If, however, you made late payments a few years ago and have had a strong history since then, they will assume you’ve gotten over hard times and are probably worth the risk. Simply put, best way to ensure this component stays high is to make your payments on any outstanding debt timely and consistent.

2. Amount of Debt (30%):

This category is where credit cards play a large role. Remember, credit cards are revolving lines of credit, meaning if my credit limit is $3,000 and I borrow $1,000 then pay back that $1,000 my credit limit is restored to its full $3,000 and the cycle continues. This type of credit is weighed very heavily when lenders look at the amount of debt you have compared to your limit. For example, if a lender sees that your limit is $3,000 and every month you max out that limit, they’re going to assume you’re not financially responsible. The best way to protect your credit score in this category is to keep a low credit card balance in regards to your limit. You should never borrow more than 50% of your credit limit on a single card. The ideal spending percent is about 30% of your credit limit. If you have multiple cards, it is better to owe smaller amounts on these cards, than to have a single card which is continuously maxed out.

3. Length of Credit History (15%):

This is the length of time any credit accounts you own have been open and in use. The longer your credit history, the easier it is for a lender to determine whether or not you are worth the risk. Someone who is just starting out in developing credit will not have a perfect credit score simply because you have not been using credit long enough. Credit cards are also not the only sources of credit and usually people with excellent credit scores have at least three sources of credit such as credit cards or installments loans. They are also usually on time with their payments and have had a credit history for at least seven years. When you start out using credit, usually with a credit card, make sure to be responsible and always pay your balance on time and in full. As you begin to accumulate more credit, it is better to keep and use old credit accounts because they have a longer and more detailed history for lenders to examine. Don’t close the account, keep it open and use it often enough to keep it active.

4. New Credit (10%):

Be cautious when opening new credit accounts. Opening too many credit accounts at the same time will make lenders assume you are experiencing hard times financially. You should only request and take on new credit when you really need it or when it makes financial sense.

5. Credit Type Mix (10%):

As mentioned in credit history, someone with an excellent credit score has more than one form of credit. This is made up of their revolving credit, credit card, and their installment credit, car and mortgage loans. Having a mix of credit sources signals to the lender that you can handle the responsibility of multiple forms of credit.

It is important to know each element of your FICO score so that you can build and improve your credit score. The general rule of thumb is to having a good credit score is to have a long positive history of credit and low balances to all your credit limits.

Let’s look at a potential real life example of making a credit decision to improve your credit score.

In this example, you have a credit card account from Monopoly Credit Union. Your current balance is $7,000 with an APR of 16% and a total credit limit of $14,000.

You receive an offer in the mail from ACE Credit Services for a credit card with a fixed APR of 8%; half of what you currently have! It sounds too good to be true! Think of all the money will save with a lower interest rate! With dollar signs flashing in your eyes you sign up for this new offer!

A week later your shiny new card arrives in the mail and you transfer your balance over to your new ACE Credit Services. You next step is essential and will greatly impact your credit score.

With your first account, Monopoly CU, you had a balance of $7,000 with a limit of $14,000 meaning you were using 50% of your available credit. 7000/14000 = 0.50 = 50%

Your new ACE card unfortunately has a credit limit of $11,000 and by switching you are now using 64% of the credit on your ACE credit card. Plus your ACE card is new and your Length of Credit will cause your FICO score to fall causing your credit score to fall.

Things would be very different if your new ACE credit card had the same credit limit as your Monopoly credit card; $14,000. Let’s say in this scenario you’ve had the Monopoly card for a few years and your payment history has been good. In this scenario, it would be better to keep your Monopoly credit card open, regardless of whether or not you are using it. By doing so, you will be using $7,000 out of a total credit of $28,000.

7000/28000 = 0.25 = 25%

Now you are using 25% of your available credit, as opposed to before when you were using 50%. This dramatic improvement should cause your credit score to go up. This does not mean the best way to build your credit score is buy opening new lines of credit. In this scenario remember there would be a balance transfer fee and taking on new debt will end up lowering your credit score for a period. If it looks like you are accumulating more credit than you need that will also lower your score.

The best way to improve your score or keep it high is to avoid any actions which will increase your debt percentage. It is better to focus on paying down your current balance and improve your debt percentage in that fashion.

Let’s look at a potential real life example of making a credit decision to improve your credit score.

In this example, you have a credit card account from Monopoly Credit Union. Your current balance is $7,000 with an APR of 16% and a total credit limit of $14,000.

You receive an offer in the mail from ACE Credit Services for a credit card with a fixed APR of 8%; half of what you currently have! It sounds too good to be true! Think of all the money will save with a lower interest rate! With dollar signs flashing in your eyes you sign up for this new offer!

A week later your shiny new card arrives in the mail and you transfer your balance over to your new ACE Credit Services. You next step is essential and will greatly impact your credit score.

With your first account, Monopoly CU, you had a balance of $7,000 with a limit of $14,000 meaning you were using 50% of your available credit. 7000/14000 = 0.50 = 50%

Your new ACE card unfortunately has a credit limit of $11,000 and by switching you are now using 64% of the credit on your ACE credit card. Plus your ACE card is new and your Length of Credit will cause your FICO score to fall causing your credit score to fall.

Things would be very different if your new ACE credit card had the same credit limit as your Monopoly credit card; $14,000. Let’s say in this scenario you’ve had the Monopoly card for a few years and your payment history has been good. In this scenario, it would be better to keep your Monopoly credit card open, regardless of whether or not you are using it. By doing so, you will be using $7,000 out of a total credit of $28,000.

7000/28000 = 0.25 = 25%

Now you are using 25% of your available credit, as opposed to before when you were using 50%. This dramatic improvement should cause your credit score to go up. This does not mean the best way to build your credit score is buy opening new lines of credit. In this scenario remember there would be a balance transfer fee and taking on new debt will end up lowering your credit score for a period. If it looks like you are accumulating more credit than you need that will also lower your score.

The best way to improve your score or keep it high is to avoid any actions which will increase your debt percentage. It is better to focus on paying down your current balance and improve your debt percentage in that fashion.

How Credit Score Impacts You

There are many ways in which your credit score can impact your daily life, below you’ll find a general list then we’ll take a closer look at some of the bigger impacts.

Credit Score Impacts:

As shown via the previous example, making responsible financial decisions can improve your credit score. Irresponsible financial decisions will do the exact opposite. Poor credit scores will hit you where it hurts, the wallet. The better your credit score, the lower the interest rate banks and other financial institutions will place when paying back loans. The lower your score, the higher your interest rate and the more expensive your loans.

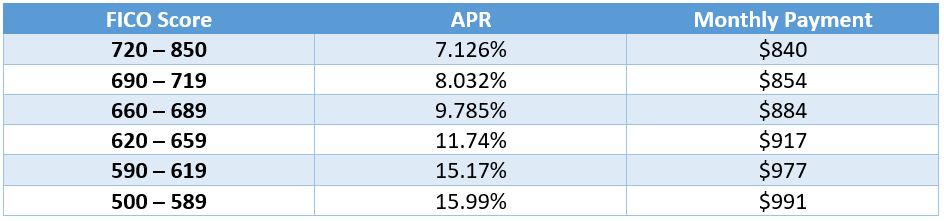

Let’s look at a FICO score to interest rate table which lenders might use when making interest rate decisions on a loan you take out. In this scenario let’s say you’re buying a car and take out an auto loan of $35,000 which is to be paid off in four years (48 months).

Credit Score Impacts:

- Your ability to attain a credit card

- Your ability to buy a home

- Whether you’ll be able to rent an apartment

- The amount of your insurance premiums

- Ability to borrow money

- Getting service from utility companies

- Getting hired

As shown via the previous example, making responsible financial decisions can improve your credit score. Irresponsible financial decisions will do the exact opposite. Poor credit scores will hit you where it hurts, the wallet. The better your credit score, the lower the interest rate banks and other financial institutions will place when paying back loans. The lower your score, the higher your interest rate and the more expensive your loans.

Let’s look at a FICO score to interest rate table which lenders might use when making interest rate decisions on a loan you take out. In this scenario let’s say you’re buying a car and take out an auto loan of $35,000 which is to be paid off in four years (48 months).

As you can see, the lower your FICO score, the more interest you will pay when paying back your loan. The higher your FICO score, you are perceived as less of a risk by the lender and will be charged a lower interest rate. The lower your FICO score, the lender will seek to balance out the risk by placing a higher interest rate on you. The chart bellow shows you how much money you will pay in interest with each APR, and monthly payment. When you pay back the loan, you're paying back the original $35,000 plus the interest.

Career Impact:

Many companies will look at a potential employee’s credit score as a factor when deciding whether to higher them. Your credit score is a representation of how responsible you are and that you can be trusted with financial decisions. As I am sure you can guess, the better your score, the more likely they are to higher you and vice versa. Of course, the impact your credit score has on potential jobs depends on the job itself. Jobs involved with payroll, senior management, accounting, or any other position in which you handle confidential information, the credit score may be a major factor in whether or not you get the job. In most cases, employers do not look at your credit score unless they are seriously considering you for the position. If you have a low credit score and some blemishes on your credit record, one option you might pursue is bringing them up in your job interview. Normally you want to just talk about how great you are right? So why does this make sense? Well, by telling your potential employer they may appreciate your honesty and it gives you a chance to explain why they are there. This is a better alternative to your employer coming to their own conclusions should they seek to look at your credit score.

Many companies will look at a potential employee’s credit score as a factor when deciding whether to higher them. Your credit score is a representation of how responsible you are and that you can be trusted with financial decisions. As I am sure you can guess, the better your score, the more likely they are to higher you and vice versa. Of course, the impact your credit score has on potential jobs depends on the job itself. Jobs involved with payroll, senior management, accounting, or any other position in which you handle confidential information, the credit score may be a major factor in whether or not you get the job. In most cases, employers do not look at your credit score unless they are seriously considering you for the position. If you have a low credit score and some blemishes on your credit record, one option you might pursue is bringing them up in your job interview. Normally you want to just talk about how great you are right? So why does this make sense? Well, by telling your potential employer they may appreciate your honesty and it gives you a chance to explain why they are there. This is a better alternative to your employer coming to their own conclusions should they seek to look at your credit score.

How You Impact Credit Score

Over the course of this section on your Credit Score I’m sure you have a good idea on how you influence your credit score. Here’s a helpful little review of what to do and not to do with your credit score.

Helping your Credit Score:

Hindering Your Credit Score

Keep all this information in mind and practice it once you first start working with credit! If you do this then over time you will be all set with building a good credit score and using credit responsibly.

Helping your Credit Score:

- Pay your bills on time and in full

- If you happen to miss a payment, work to get current and stay current

- Use 33% of your spending limit; 50% maximum

- Pay down credit card balance to improve debt percentage

- Keep your balance low!

- A steady employment history

- Only applying for a credit card when you need it

- Don’t apply for a new account just to improve debt percentage

- A good credit history over a long period of time

- Don’t close old accounts – use them occasionally and pay them off monthly

- Finally: BE RESPONSIBLE WITH YOUR CREDIT

Hindering Your Credit Score

- Late bill payments

- Credit card balances near your spending limit

- Applying for new credit cards frequently without a real need for it

- A short credit history

- Exceeding your credit limit

Keep all this information in mind and practice it once you first start working with credit! If you do this then over time you will be all set with building a good credit score and using credit responsibly.