What is Credit?

|

Credit: Making a purchase with the promise that the money used will be paid back later

Curious to see how your state ranks nationally on managing and fulfilling credit obligations? Check out this nifty interactive map by Federal Reserve Bank of New York. |

Credit Cards vs. Debit Cards

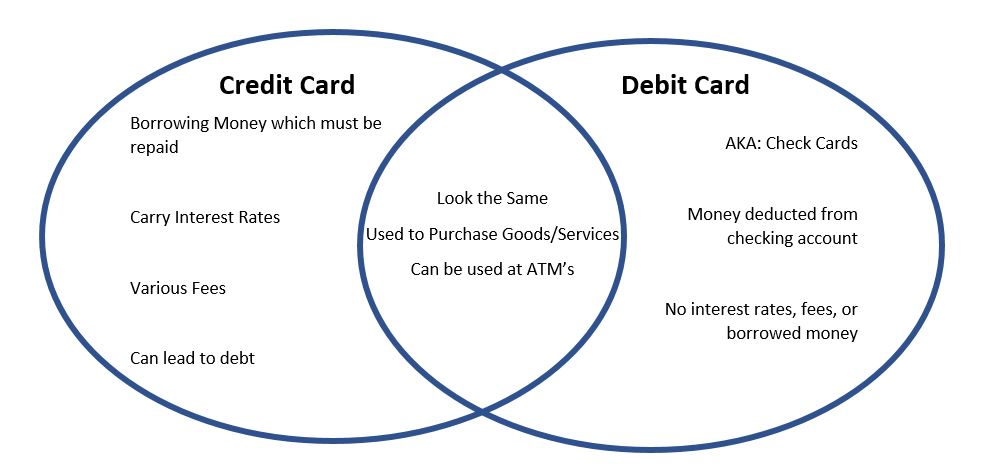

You may find that most people, maybe even yourself have both of these, but what's the difference between them? A credit card is a card issued by a bank or business which allows the holder to borrow funds to purchase goods. A debit card is a card used to purchase goods or services which takes money directly from the user's checking account. See the difference? With the credit card, you're using credit to borrow money and make purchases. With a debit card, you're using your own money to pay for the good or service.

Here's a handy little Venn Diagram:

Here's a handy little Venn Diagram:

Purchasing with a Credit Card

As stated above, you are borrowing credit to pay for purchases. Every month you must pay back the credit you borrowed using money from your bank account. It's a buy now, pay later scenario. If you don't make your payments, interest will built which can lead you into debt. When purchasing with a credit card it is important to remember how much money you have in the bank so you don't spend more than you can pay back. Using and owning a credit card is a privilege and there are many responsibilities which go hand in hand with using it.

When purchasing with the card, there are three factors to keep in mind: credit limit, charging, and interest rate. The credit limit is the maximum amount of money that the credit issuer will allow you to charge to that card (aka line of credit). The charge is the money you borrow when you use the card. Finally, the interest rate is the percentage you pay on the money you have charged to the card. This is extremely important when it comes to a late payment.

When it comes time to pay back what you've borrowed, you are presented with two options. Option one, pay in full, meaning I pay off the entirety of what I owe. By doing so, I will not be charged interest and my credit limit is restored back to it's full amount. Someone who pays off their entire balance at the end of the month and never pays a late fee is known as a deadbeat by credit card companies. Option two, make a minimum payment meaning I pay the minimum amount possible to let the credit card company know you don't quite have the money right now, but will pay it back. The money you still owe when a full payment is not made is known as an outstanding balance.

By paying the minimum or some other amount lower than what you owe, you begin a process known as "carrying the balance", meaning you are carrying your outstanding balance into the next billing cycle. If you make your payment in full and don't carry your balance, credit card companies will give you a grace period. The grace period is the length of time between the use of credit to make a purchase and start of interest on the amount charged. During this window of time, you the consumer owes money to the credit card company for new purchases but you aren't being charged interest. You lose this period when you make a minimum payment and carry your balance.

When purchasing with the card, there are three factors to keep in mind: credit limit, charging, and interest rate. The credit limit is the maximum amount of money that the credit issuer will allow you to charge to that card (aka line of credit). The charge is the money you borrow when you use the card. Finally, the interest rate is the percentage you pay on the money you have charged to the card. This is extremely important when it comes to a late payment.

When it comes time to pay back what you've borrowed, you are presented with two options. Option one, pay in full, meaning I pay off the entirety of what I owe. By doing so, I will not be charged interest and my credit limit is restored back to it's full amount. Someone who pays off their entire balance at the end of the month and never pays a late fee is known as a deadbeat by credit card companies. Option two, make a minimum payment meaning I pay the minimum amount possible to let the credit card company know you don't quite have the money right now, but will pay it back. The money you still owe when a full payment is not made is known as an outstanding balance.

By paying the minimum or some other amount lower than what you owe, you begin a process known as "carrying the balance", meaning you are carrying your outstanding balance into the next billing cycle. If you make your payment in full and don't carry your balance, credit card companies will give you a grace period. The grace period is the length of time between the use of credit to make a purchase and start of interest on the amount charged. During this window of time, you the consumer owes money to the credit card company for new purchases but you aren't being charged interest. You lose this period when you make a minimum payment and carry your balance.

Purchasing with a Debit Card

The money spent with a credit card is your own money, no borrowing or paying back involved. With this set up technically you cannot go into debt. The only case where a debit card will lead to debt is by making a purchase and drawing funds from an account with a negative balance.

Risks and Benefits

Should you get a credit card? What are the risks and benefits of owning a credit card? Though credit cards can lead to debt, they do have some benefits as well. Here is a simple list of the risks and benefits to owning a credit card.

Benefits:

Risks

Benefits:

- If you maintain good credit it is easier to rent apartments and attain service from various local utility companies.

- Good Credit allows for the option of buying items now and paying the money back over time as opposed to waiting until you have the cash.

- Going off that, it’s easier to buy what you want, when you want it. Yay instant gratification!

- You have the means to make a larger financial purchase which requires more money than you have on hand.

- Allows you to act on life opportunities, like attaining an education at a good college or university!

- Some credit cards provide rewards whether it’s travel, cash back, or redeemable points! Cool stuff!

Risks

- Credit makes it easier to spend more, spending more than you have leads to debt, interest payments, and late fees.

- Failing to make loan payments can hurt your credit record. Should you have a poor credit record, you could be turned down for renting an apartment or even attaining a job!!

- Low credit ratings and a large outstanding balance makes it harder to get loans and credit come next month. Even with the credit you attain you’re paying high interest.

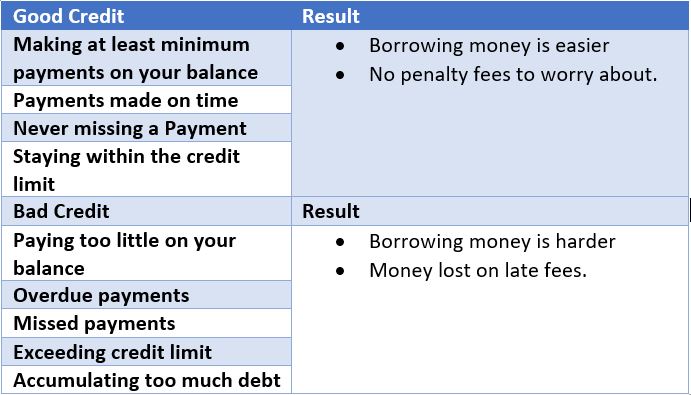

Good Credit vs. Bad Credit

Here’s the simple version: Good Credit means you’ve been making your payments on time and in full. Bad Credit is failing to make payments on time and in full. Here’s a handy little chart to keep in mind when looking for signs of good and bad credit:

Keeping Your Credit Secure

These are some things to keep in mind and/or do to keep your credit safe. Some of these may seem like common sense, but it's good to be reminded once and a while.

- Never give your card to anyone – you don’t want someone else making charges to your card.

- Never sign a blank charge slip. If you leave blank spaces on a charge slip, make sure to draw a line in them so that no one may go back and change the amount.

- Never put your account number on an envelope or post card

- Use caution when disclosing your account number via the telephone, online, or some other communication device. Make sure you know the person with whom you are dealing with and that they are representing a trustworthy company.

- Keep all receipts and print out all online receipts and compare them to your bill.

- Should you have more than one credit card, carry only the ones you use the most to reduce the damage should you lose one or get robbed.

- In a safe place, away from your credit cards, keep a record of all account numbers, expiration dates, and phone numbers for each creditor so that you can report a loss quickly.

- Check your credit report once a year for any errors or mistakes, which if found should be reported immediately!